Deciding to seek debt relief is a significant crossroad that many individuals and small business owners face when financial obligations become insurmountable. In the specific economic climate of Southern California, where the cost of living and housing market volatility can create unique pressures, understanding the structured path toward a fresh start is essential.

The process is governed by federal law, yet it is heavily influenced by local California exemptions and court procedures. Navigating this journey typically involves a series of mandatory phases designed to ensure transparency, fairness to creditors, and a sustainable outcome for the debtor. Engaging a bankruptcy attorney San Diego is often the first step in ensuring these phases are executed without procedural errors that could lead to a dismissed case.

Initial Assessment and Determining the Correct Chapter

The first and most critical step is a comprehensive audit of your financial standing. This phase determines whether you qualify for liquidation or a reorganization plan.

The Means Test Requirement

To file for Chapter 7—which allows for the discharge of most unsecured debts—you must pass the “Means Test.” This calculation compares your average monthly income over the last six months to the median income for a household of your size in California. If your income is below the median, you automatically qualify. If it is above, a more complex calculation of allowed expenses is required to determine if you have enough “disposable income” to pay back some portion of your debt.

Choosing Chapter 13

If you do not pass the Means Test, or if you are specifically looking to save a home from foreclosure or a vehicle from repossession, Chapter 13 is often the preferred route. This chapter involves a three-to-five-year repayment plan where you pay a portion of your debts based on what you can afford, while protecting your primary assets from liquidation.

Mandatory Credit Counseling

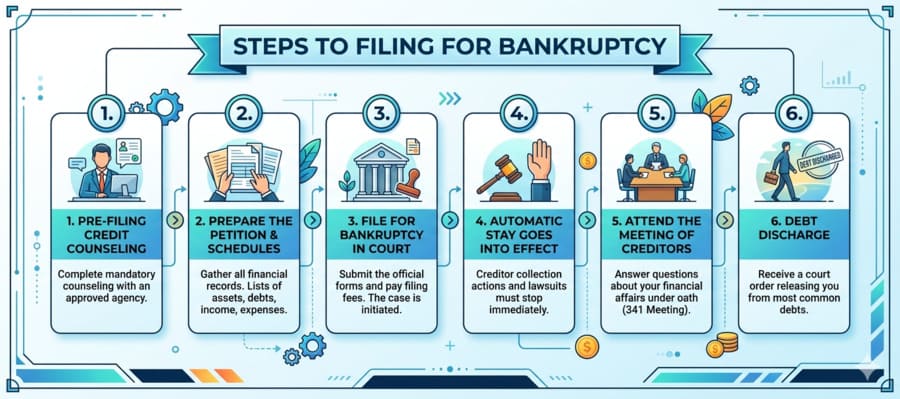

Before any paperwork can be filed with the U.S. Bankruptcy Court for the Southern District of California, the law requires you to complete a credit counseling course from an approved agency.

- Timeline: This must be completed within 180 days before your filing date.

- Purpose: The goal is to ensure that you have explored all alternatives to bankruptcy, such as debt management plans, before proceeding with a formal filing.

Gathering Documentation and Preparing the Petition

Filing for debt relief requires a level of financial disclosure that can be overwhelming without professional guidance. A legal representative in Southern California will typically require a “master folder” of your financial life, including:

- Tax returns from the last two to four years.

- Pay stubs and proof of all income sources (including rental income or side hustles).

- A complete list of all creditors, including those you intend to keep paying (like a car loan).

- A detailed inventory of everything you own, from real estate and retirement accounts to household furniture.

This information is used to populate the “Schedules” of your bankruptcy petition, which is the official document submitted to the court.

The Automatic Stay and the Role of the Trustee

Once your petition is filed, a powerful legal injunction known as the “Automatic Stay” goes into effect. This immediately halts almost all collection actions, including:

- Harassing phone calls and letters.

- Wage garnishments.

- Pending lawsuits.

- Foreclosure proceedings and repossessions.

Shortly after filing, the court will appoint a Bankruptcy Trustee. In a Chapter 7 case, the Trustee’s job is to review your assets and determine if anything can be sold to pay creditors. In a Chapter 13 case, the Trustee oversees your repayment plan and distributes your monthly payments to the creditors.

Attending the Meeting of Creditors (341 Meeting)

Approximately 30 to 45 days after your filing, you must attend the Meeting of Creditors. While the word “meeting” sounds informal, this is a legal proceeding where you are under oath.

- The Process: The Trustee will ask a series of questions to verify the accuracy of your petition.

- Creditor Participation: While creditors are invited to attend and ask questions, in the vast majority of consumer cases, they do not appear.

Having a bankruptcy attorney in San Diego by your side during this meeting is vital for ensuring that your answers are precise and that your rights are protected throughout the questioning.

Applying California Exemptions to Protect Assets

One of the most complex parts of filing in Southern California is choosing between the two sets of exemptions offered by the state. California does not allow you to use federal exemptions; instead, you must choose between “System 1” (often better for homeowners with equity) and “System 2” (often better for those with significant cash, tools of the trade, or “wildcard” needs).

- The Homestead Exemption: This is particularly important for residents in high-value areas like La Jolla or Chula Vista. The exemption protects a specific amount of equity in your primary residence from being used to pay off creditors.

- Personal Property: Exemptions also cover items like your primary vehicle, clothing, and necessary household goods up to certain dollar limits.

Financial Management Course and Discharge

After your 341 Meeting, and before your case can be closed, you must complete a second education course: the Debtor Education/Financial Management course. This focuses on budgeting and responsible credit use to help ensure you do not find yourself in financial distress again.

In a Chapter 7 case, if no objections are filed, the court will issue a Discharge Order roughly 60 to 90 days after your meeting. This order legally releases you from personal liability for the discharged debts. In Chapter 13, the discharge is granted after you complete all payments in your court-approved plan.

Moving Forward with a Fresh Start

Filing for bankruptcy is a technical process, but the ultimate goal is human: the restoration of peace of mind. By following these essential steps and utilizing the protections provided by the California legal system, you can resolve the weight of the past and begin building a more stable financial future.